Cross-border VAT e-commerce is being updated in the EU from 1th July 2021

Who is affected about thi? From online merchants and marketplaces/platforms both inside and outside the EU, through postal operators and couriers, customs and tax agencies, and consumers, everyone in the e-commerce supply chain is affected. So, what’s new? The VAT regulations for cross-border business-to-consumer (B2C) e-commerce activity will change on July 1, 2021. The aim […]

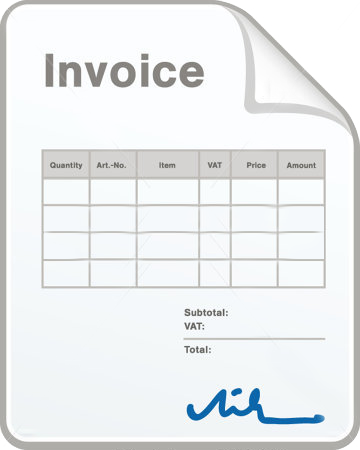

How to do a Proforma and Commercial Invoices for import or export

Usually, when the importer and the potential clients are surely satisfied with the quality of their products, the delivered samples, time of the package/delivered are tested and the price are acceptable. They will offer you a confirmed offer. This article gives extended information regarding our ex-products. Proforma invoices, comercial invoices and export documentations. What will […]

How to import in Spain for NON European companies, Create new company in Spain and Get your EORI and file your tax returns

This article has been wrote specially for Non EU companies interested to import in Spain or Europe. Amazon, Ebay, Etsy sellers or project initiators at Kickstarter, Indiegogo, etc. aiming to sell to EU individuals you may be aware of the following points. INTRODUCTION : Import : introducing goods to EU territory means you will be […]

Everything about VAT when importing at Europe for Ecommerce International sellers

Selling Internationally? Everything You Need TO LEARN About taxes at Europe With the growth of the global e-commerce scenery and a shift in shopping habits, an increasing number of retailers of most sizes are discovering that expanding internationally is an exciting and natural probability. International expansion poses many opportunities, including a vast number of new […]

Custom bonded warehouse DA and fiscal warehouse DDA or how to import into Europe avoid import taxes

The DDA licence (Fiscal warhouse or VAT Warehouse) is one of the most versatile and interesting for companies that needs to import in Europe Spainbox owns a tax warehouse, duly licensed by the Spanish authorities, which enables companies to conduct purchase or sale operations without having to pay Value added taxes (VAT, IVA in Spanish) at the time of purchase […]

9 Tips to import clothes from Spain to non-EU countries and reduce customs fees

international shoppers prefer to buy fast fashion in Spain, at Zara, Mango, bershka, Pull and Bear, Massimo Dutti etc. because it is cheaper to buy from Spain.

This tips will help you to reduce the customs fees in the destination country or even your recipient does not have to pay duties and taxes when the clothing is received at the destination outside the country out of the european union.